Good grief ~ I am a smart gal ~ what is my hang up with IRR? Here is my deal:

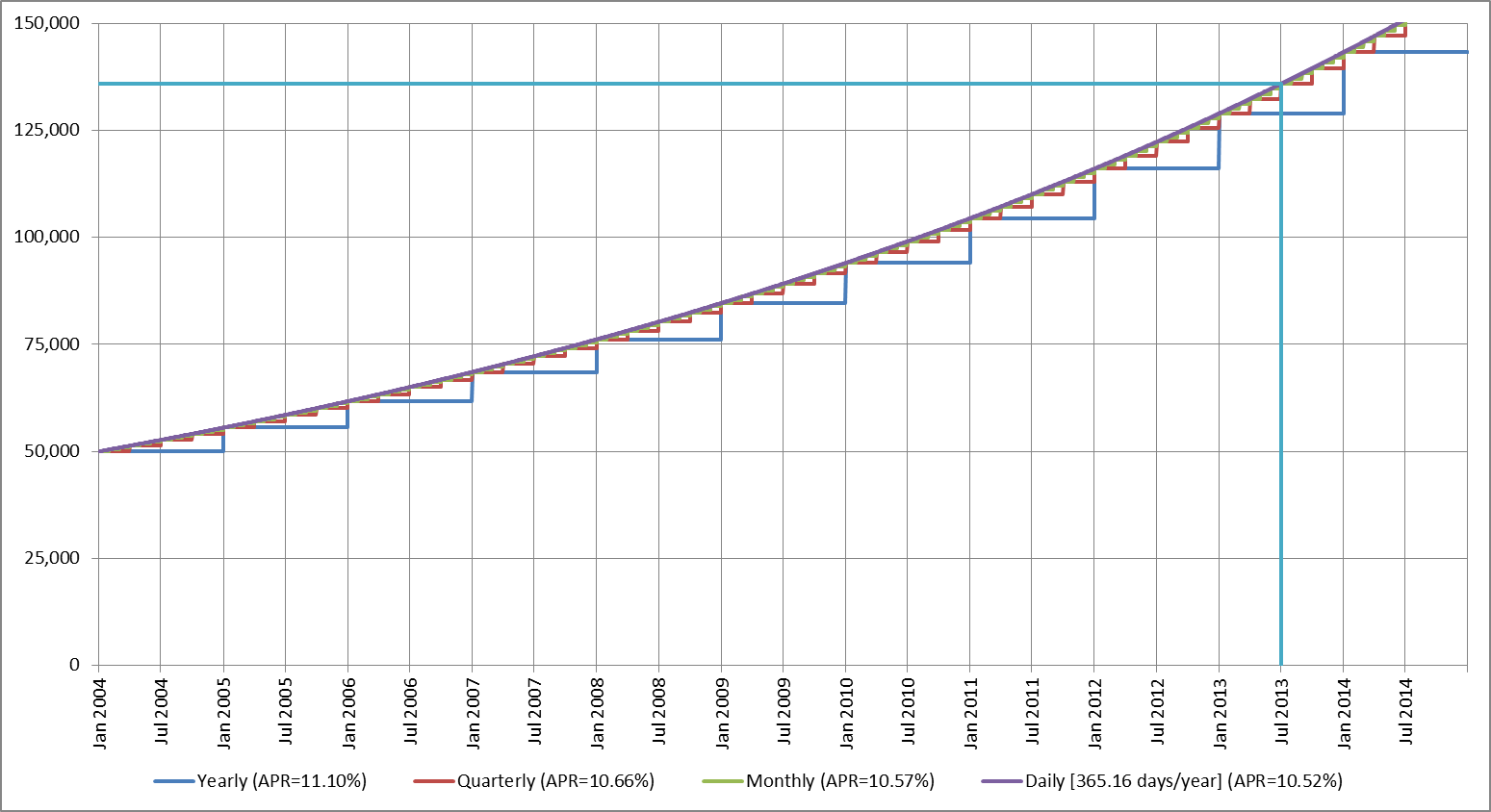

I have monthly % return data for 9.5 years for an investment. I want to determine the AVERAGE ANNUAL RATE OF RETURN. but I can’t figure it out!!!!!!

Investment begins with $50,000; Value after 9.5 years is $135,869.62

please help!!!

{kind=link}